Singapore Economic Outlook Q1 2026: Navigating Growth Amid Global Uncertainty

By Jerry Tan of Tangent Human Capital on 29 Dec 2025

As we enter the first quarter of 2026, Singapore stands at a critical juncture in its economic trajectory. After experiencing robust growth of approximately 4% in 2025, the city-state is expected to moderate to a more sustainable pace as global headwinds intensify and geopolitical tensions reshape international trade dynamics.

Economic Growth Projections

Singapore’s Ministry of Trade and Industry (MTI) projects GDP growth of between 1% and 3% for 2026, with most economists converging on estimates around 1.8% to 2.7%. This represents a significant deceleration from 2025’s performance but remains within the government’s near-trend growth expectations. The Monetary Authority of Singapore (MAS) anticipates that the output gap will narrow to around 0% by year-end, suggesting the economy is moving toward equilibrium after the post-pandemic recovery phase.

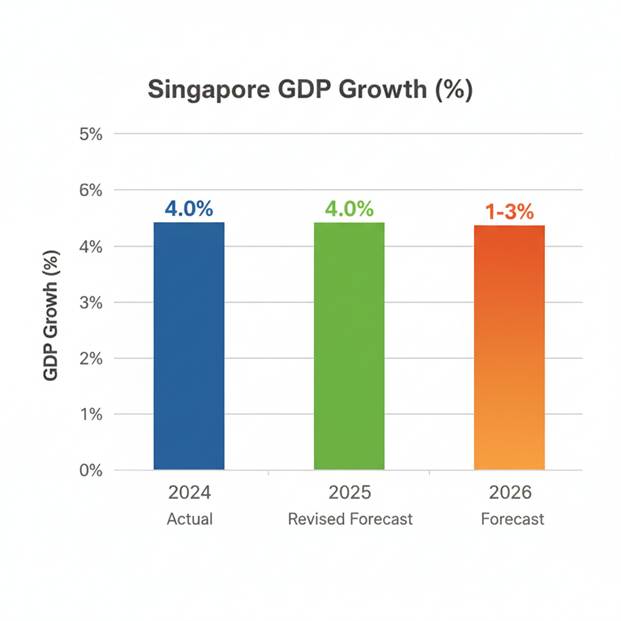

2024 (Actual): 4.0% GDP growth

- Source: Ministry of Trade and Industry (MTI), official press release, January 2025

2025 (Revised Forecast): Around 4.0% GDP growth (upgraded from 1.5-2.5%)

- Source: MTI press release, November 21, 2025

- Context: Upgraded after Q3 2025 actual growth of 4.2% beat advance estimates of 2.9%

2026 (Forecast): 1% to 3% GDP growth range

- Source: MTI maiden forecast for 2026, announced November 21, 2025

- Context: Expected moderation due to global headwinds, US tariff impacts, and normalization after strong 2025 performance

Singapore GDP Growth Forecast

This moderation reflects several factors. The electronics cycle, which provided substantial momentum in 2024 and 2025, is expected to normalize. Additionally, global demand is projected to soften as major economies adjust to higher interest rates and structural economic shifts. Singapore’s highly open economy, with trade exceeding three times its GDP, makes it particularly sensitive to these external developments.

Growth Sectors: Where Opportunity Thrives

Despite the overall slowdown, several sectors are positioned for continued expansion in Q1 2026 and beyond. Understanding these growth areas is crucial for businesses and job seekers looking to capitalize on emerging opportunities.

- Technology and Digital Services remain the cornerstone of Singapore’s economic strategy. The IT and information services segment continues to attract substantial investment, with the technology sector generating approximately 50% of revenue for specialized recruitment firms like those focused on corporate functions. Demand for digital workers is expected to increase significantly, driven by ongoing digital transformation initiatives across industries. Cloud computing, cybersecurity, artificial intelligence, and data analytics professionals are particularly sought after.

- Green Economy and Sustainability sectors are experiencing accelerated growth as Singapore positions itself as a regional hub for sustainable finance and clean technology. The government’s commitment to achieving net-zero emissions by 2050 is driving investment in renewable energy, carbon services, and environmental technologies. This transition is creating new employment opportunities in areas such as sustainability consulting, green finance, and environmental engineering.

- Biomedical Sciences and Healthcare continue their upward trajectory, supported by Singapore’s established pharmaceutical manufacturing base and growing research capabilities. The aging population across Asia is driving demand for healthcare services, medical devices, and pharmaceutical innovations. Precision medicine and biotechnology are particularly promising subsectors receiving government support and private investment.

- Financial Services maintain their resilience, with Singapore’s status as a global financial center continuing to attract wealth management, fintech innovation, and institutional banking activities. The sector benefits from regional economic growth and Singapore’s stable regulatory environment, even as global financial conditions tighten.

- Professional Services, including recruitment, HR consultancy, legal services, and business consulting, show sustained demand. Organizations navigating economic uncertainty require expert guidance on workforce optimization, compliance, and strategic transformation.

Sectors Facing Headwinds

While certain industries thrive, others confront significant challenges in the Q1 2026 environment. Recognizing these pressures is essential for strategic planning and risk management.

- Traditional Manufacturing faces mounting pressure from automation requirements, rising costs, and global overcapacity in certain segments. The sector confronts an aging workforce, and companies must invest heavily in Industry 4.0 technologies to remain competitive. Middle-skilled manufacturing jobs are declining as automation advances, creating a polarization in the labor market.

- Trade-Related Industries are particularly vulnerable to the global tariff environment and supply chain reconfigurations. Singapore’s role as a transshipment hub faces challenges as companies reassess their logistics networks in response to geopolitical tensions. The reversal of export front-loading that occurred in late 2025 is expected to create headwinds in early 2026.

- Traditional Retail continues its structural decline as e-commerce penetration deepens. Physical retail spaces face pressure from changing consumer preferences and the convenience of digital platforms, though experiential retail and luxury segments show more resilience.

- Construction activity is moderating after several years of strong growth, with both public and private sector projects facing completion. The sector must also navigate labor constraints and sustainability requirements that increase project complexity and costs.

Geopolitical Landscape and Economic Implications

The geopolitical environment in Q1 2026 presents both risks and opportunities for Singapore’s economy. Understanding these dynamics is crucial for anticipating market shifts and strategic positioning.

Geopolitical Impacts

US-China Trade Tensions remain the dominant geopolitical factor affecting Singapore. Escalating tariffs and technology restrictions create uncertainty for multinational corporations operating in the region. However, Singapore would benefit from supply chain diversification as companies seek neutral locations for regional headquarters and manufacturing operations. The challenge lies in maintaining balanced relationships with both powers while preserving Singapore’s role as a trusted business hub.

ASEAN Integration offers a counterbalance to global fragmentation. Deeper economic integration within Southeast Asia creates opportunities for Singapore-based companies to serve the region’s growing consumer markets. Five of ASEAN’s six largest economies currently enjoy trade surpluses with the United States, making the region vulnerable to potential tariffs but also highlighting its export competitiveness.

Supply Chain Reconfiguration is accelerating as companies prioritize resilience over pure cost optimization. This “China Plus One” strategy benefits Singapore as companies establish regional operations centers and diversify their manufacturing footprint across Southeast Asia. Singapore’s infrastructure, legal framework, and skilled workforce position it advantageously to capture coordination and high-value activities.

Regional Stability Concerns in the South China Sea and broader Indo-Pacific create ongoing uncertainty. While Singapore maintains neutrality, any escalation could disrupt trade flows and investment sentiment. The city-state’s emphasis on multilateral engagement and rules-based international order reflects its vulnerability to regional instability.

Job Market Dynamics in Q1 2026

The employment landscape reflects the broader economic transition, with significant variation across sectors and skill levels. Understanding these trends is essential for talent acquisition and career planning.

The Net Employment Outlook for Q1 2026 shows cooling from previous quarters, with employers adopting a more cautious stance. Hiring activity remains selective but stable, with companies focusing on critical roles and high-impact positions rather than broad-based expansion. This environment favors candidates with specialized skills and proven track records.

In-Demand Roles cluster in growth sectors. Technology positions, particularly in cybersecurity, cloud architecture, data science, and AI development, command premium compensation. Green economy roles in sustainability consulting, ESG reporting, and renewable energy are emerging as high-growth areas. Healthcare professionals, including specialized nurses, medical technologists, and healthcare administrators, face strong demand driven by demographic trends.

Finance sector hiring focuses on wealth management, risk management, and fintech expertise. Professional services firms seek consultants with digital transformation, change management, and industry-specific expertise. Notably, the Ministry of Manpower’s Shortage Occupation List for 2026 highlights critical needs across green economy, finance, and healthcare sectors.

Time-to-Fill Metrics vary significantly by role complexity. Junior positions typically fill within two to four weeks, mid-level roles require three to six weeks, and senior executive searches extend to four to eight weeks. The selective hiring environment means companies are taking longer to evaluate candidates and ensure cultural fit alongside technical capabilities.

Skills Evolution is perhaps the most significant trend. Employers increasingly adopt skill-first hiring approaches, prioritizing demonstrable capabilities over traditional credentials. This shift creates opportunities for career changers and non-traditional candidates who can prove their competencies. Continuous learning and adaptability have become essential attributes across all sectors.

Strategic Implications for Businesses

Organizations operating in or entering the Singapore market in Q1 2026 should consider several strategic imperatives. The moderated growth environment rewards agility, specialization, and strategic workforce planning.

Companies should focus on productivity enhancement through technology adoption rather than headcount expansion. Investments in automation, data analytics, and digital tools can maintain output while managing costs. This approach aligns with Singapore’s national productivity agenda and available government support programs.

Talent strategies must balance cost management with the need to attract critical skills. Flexible work arrangements, including contract and project-based talent solutions, provide agility in uncertain times. Retention of high performers becomes paramount as selective hiring makes replacement more challenging and time-consuming.

In Conclusion: Cautious Optimism for Q1 2026

Singapore enters Q1 2026 with a mature, realistic outlook. The anticipated growth moderation to 1.8% to 2.7% reflects global realities rather than domestic weaknesses. The city-state’s diversified economy, strong institutions, and strategic positioning provide resilience against external shocks.

Success in this environment requires discernment. Growth sectors in technology, green economy, biomedical sciences, and professional services offer genuine opportunities for expansion and employment. Conversely, traditional manufacturing, trade-dependent industries, and conventional retail face structural headwinds requiring transformation or strategic repositioning.

The job market reflects this complexity regarding geopolitical tensions, with strong demand for specialized skills coexisting with cautious overall hiring. Employers and job seekers alike must embrace continuous learning, flexibility, and strategic positioning to thrive.

For businesses and professionals who navigate these dynamics thoughtfully, Q1 2026 presents one of strategic opportunity. Those who invest in the right capabilities, sectors, and partnerships will emerge stronger as global conditions eventually stabilize and growth accelerates in subsequent years.